The allure of high yields in Decentralized Finance (DeFi) lending has attracted a wide range of investors, from seasoned entrepreneurs to tech-savvy individuals and business owners seeking better returns. As of early 2025, over $100 billion is locked in DeFi lending protocols, marking a significant increase from previous years, driven by growing institutional interest and improved platform security. However, the risks are equally pronounced.

For instance, a business owner, enticed by attractive annual percentage yields (APYs), deposited a substantial portion of their company’s crypto assets into an unaudited smart contract, only to lose everything due to a critical coding flaw. This wasn’t merely a setback it was a stark reminder of the hidden dangers in decentralized finance. This guide provides a detailed examination of the risks associated with DeFi lending, offering insights and solutions to help you navigate this innovative yet perilous financial ecosystem with caution and clarity.

DeFi Lending: The Core Concepts

DeFi lending platforms are revolutionizing finance by offering a decentralized alternative to traditional banking. Instead of relying on intermediaries, these platforms use self-executing code to connect lenders and borrowers directly. This peer-to-peer model promises greater efficiency and control, but understanding its foundational elements is crucial to grasping the inherent risks in decentralized finance lending.

Smart Contracts Explained

Smart contracts are the backbone of DeFi lending, acting as both the rulebook and the referee. These self-executing agreements, written in code and deployed on a blockchain, automatically enforce the terms of lending and borrowing. They dictate everything from interest rates and collateral requirements to the intricacies of liquidation processes.

Platforms like Aave and Compound are prime examples of how smart contracts power decentralized lending. However, the security and reliability of these platforms are directly tied to the quality of their underlying code. A flaw in the code can be exploited, often with irreversible consequences. For instance, in 2023, over $1.5 billion was lost to smart contract exploits, highlighting the importance of rigorous audits and security measures.

Read More: What Assets Can Be Tokenized?

Liquidity Pools: The Fuel Supply

Liquidity pools are essential to DeFi lending, allowing users to lend assets and earn interest based on supply and demand algorithms. While this model enables efficient borrowing and lending, it carries risks—particularly impermanent loss. When asset prices shift significantly, the pool adjusts to maintain balance, which can lead to reduced holdings of higher-performing assets like Ether. In 2024, impermanent loss remained a major risk factor, especially during periods of high market volatility, with some liquidity providers facing notable losses despite earning trading fees.

Decentralized Protocols: The Operating System

DeFi lending platforms rely on decentralized protocols like MakerDAO and Uniswap, which serve as their foundational infrastructure. These protocols operate through community governance or predefined algorithms, aiming to create a transparent and democratic alternative to traditional finance.

To properly assess the risks, users must understand each protocol’s mechanisms—such as collateral requirements, liquidation rules, and governance models. For instance, MakerDAO enforces over-collateralization (typically 150%) to help maintain stability during market volatility.

Read More: What Assets Can Be Tokenized?

Key Risks in DeFi Lending: Spotting the Red Flags

While the allure of high returns can be captivating, a thorough understanding of the potential pitfalls is non-negotiable for anyone venturing into DeFi lending. Let’s delve into the inherent risks of DeFi lending platforms, equipping you with the knowledge to spot the red flags.

Smart Contract Exploits: When Code Fails

Smart contract exploits remain a fundamental threat in the DeFi space. Despite rigorous testing and audits, vulnerabilities persist in the code governing these platforms. In 2024 alone, $2.3 billion was lost due to smart contract vulnerabilities, with 65% of DeFi-related breaches attributed to these flaws. These vulnerabilities, when exploited by malicious actors, can lead to fund draining, balance manipulation, or platform integrity compromise. The immutable nature of blockchain ensures that once exploited, transactions are irreversible, underscoring the importance of selecting platforms with a proven security track record and thorough auditing processes.

Even platforms audited by reputable firms like ConsenSys Diligence are not immune. For instance, in 2024, 90% of audited smart contracts still had critical or major vulnerabilities before deployment, highlighting the ongoing need for vigilance and continuous security improvements. Recent advancements in AI-driven auditing tools, such as CertiK, have improved vulnerability detection accuracy to 96%, but the complexity of exploits, like flash loan attacks and oracle manipulation, continues to challenge the ecosystem.

Read More: What Assets Can Be Tokenized?

Flash Loan Attacks: Exploiting the Speed of Light

Flash loan attacks represent a sophisticated threat in the decentralized finance (DeFi) landscape, exploiting the unique properties of flash loans uncollateralized loans that must be borrowed and repaid within a single blockchain transaction. Attackers utilize these rapid loans to manipulate market prices or exploit vulnerabilities in smart contracts, all within the confines of one transaction block.

The 2023 Curve Finance hack, which resulted in losses exceeding $73.5 million, exemplifies the risks associated with flash loan attacks. This incident was attributed to a hidden compiler bug in the Vyper programming language, which led to vulnerabilities across multiple liquidity pools. While white-hat hackers and MEV bots attempted to recover funds during the attack, the event underscored the critical need for enhanced smart contract security measures.

Similarly, in May 2023, the Exactly Protocol suffered an exploit that resulted in losses of around $7.3 million. This attack also involved a flash loan, demonstrating how attackers can leverage such financial instruments to capitalize on existing vulnerabilities.

Overall, flash loan attacks have caused significant financial damage within the DeFi sector, with estimates indicating over $200 million lost due to such exploits in 2023 alone. The ongoing evolution of DeFi protocols continues to present new vulnerabilities, emphasizing the necessity for robust security practices and vigilant monitoring of smart contract integrity.

Impermanent Loss: The Hidden Cost of Liquidity

Impermanent loss is a key but often overlooked risk for liquidity providers on decentralized finance (DeFi) lending platforms, particularly those using automated market makers (AMMs) on decentralized exchanges (DEXs). It occurs when the value of assets in a liquidity pool changes due to price fluctuations, often resulting in holding more of the depreciating asset and less of the appreciating one—leading to lower returns than simply holding the assets.

Though called “impermanent,” this loss becomes real when funds are withdrawn during price imbalance. Because crypto markets are highly volatile, impermanent loss remains a serious concern. However, it can be partially offset by trading fees in high-volume pools and mitigated through strategies like using stablecoin pools, timing market entries, and diversifying across assets. Some DEXs also use dynamic fee models to help reduce the impact.

Effectively understanding and managing this risk is crucial for anyone providing liquidity in DeFi lending environments.

Read More: What Assets Can Be Tokenized?

Liquidity Risk: When Exiting Becomes a Challenge

Liquidity risk in decentralized finance (DeFi) lending refers to the potential difficulty in converting assets back into cash or other cryptocurrencies when needed. This risk can arise in several scenarios:

Low Trading Volume: On platforms with limited trading activity, users may struggle to sell their tokens at a fair price or withdraw funds promptly due to a lack of buyers or reserves. As DeFi protocols like Aave, Compound, and MakerDAO gain traction, the importance of liquidity pools becomes evident, as they facilitate borrowing and lending by ensuring capital availability.

Market Volatility: During periods of extreme market fluctuations or panic selling, many users may attempt to withdraw their funds simultaneously. This can lead to network congestion, resulting in delays or even temporary freezes on withdrawals. The volatile nature of cryptocurrencies exacerbates this issue; for instance, the annualized volatility of Bitcoin and Ether has been significantly higher than that of traditional assets like the Euro Stoxx 50.

Over-Collateralization: DeFi lending typically requires borrowers to provide collateral exceeding the loan amount to mitigate default risk. However, if the value of this collateral drops sharply, users may face liquidation, risking the loss of their assets.

When it comes to the risk of DeFi lending platforms, a useful comparison is trying to sell a large amount of a low-liquidity stock during a market crash — it’s hard to find buyers without accepting major losses. Similarly, DeFi users must choose well-established platforms with strong liquidity and stay alert to broader market events that may limit fund access. As DeFi evolves, recognizing these risks is essential for both lenders and borrowers to operate safely.

Regulatory Risk: The Unfolding Legal Landscape

Regulatory uncertainty poses a major threat to DeFi lending platforms. As governments and regulators worldwide struggle to define and oversee the DeFi space, the absence of clear rules casts doubt on the long-term legality and stability of these platforms. Potential outcomes range from stricter KYC/AML compliance to full bans in certain regions.

Ongoing debates—such as whether cryptocurrencies should be treated as securities—could greatly affect both platforms and users. While regulation might improve user safety, it could also hinder innovation and compromise DeFi’s core principle of decentralization. For now, both developers and users must navigate a shifting and unpredictable regulatory landscape.

Read More: What Assets Can Be Tokenized?

Rug Pulls: The Vanishing Act

Rug pulls remain a significant threat in the decentralized Finance (DeFi) ecosystem, representing a form of exit scam where developers abandon a project and abscond with investors’ funds. This malicious tactic has become alarmingly prevalent, accounting for a substantial portion of cryptocurrency scam revenue in recent years. In 2021, rug pulls were responsible for approximately 37% of all scam-related losses, totaling over $2.8 billion.

A notable example is the AnubisDAO incident, which occurred in October 2021. In this case, developers raised around 13,556 ETH, valued at approximately $60 million, only to vanish shortly after the funds were deposited. Investigations revealed suspicious transactions linked to this incident, indicating that the stolen funds were moved through various addresses and potentially laundered using cryptocurrency mixers. Despite extensive blockchain analysis, the true identities of the perpetrators remain elusive.

Another infamous case is the Meerkat Finance incident from 2021, where about $31 million was reportedly stolen in a similar fashion. The ongoing evolution of rug pull strategies highlights the need for investors to exercise extreme caution. Identifying potential scams requires careful scrutiny of projects, particularly those with anonymous teams, unaudited code, or promises of unrealistic returns.

As of early 2025, the DeFi landscape has seen a surge in rug pull incidents, with reports indicating that there were numerous incidents in a single day alone, resulting in cumulative losses for that month reaching millions. The increasing sophistication of these scams poses a serious risk to the integrity of the DeFi market. Experts emphasize that vigilance and due diligence are essential for investors navigating this volatile space.

Market Volatility: Riding the Crypto Coaster

Market volatility is a core risk in DeFi lending. Sudden price swings in cryptocurrencies can lead to collateral liquidation for borrowers and default risk for lenders. These sharp fluctuations make it difficult to predict returns and require strong risk management skills. DeFi participants must be prepared for a highly unpredictable environment, similar to riding a financial rollercoaster.

Operational Risks: When the Machine Breaks Down

DeFi lending platforms face significant operational risks, ranging from ineffective decentralized governance to potential mismanagement by core teams. These issues can delay critical decisions, weaken security, or impair platform functionality. Additionally, users face personal risks, such as losing access to funds due to compromised or lost private keys. Just like with any complex tech system, without strong oversight and secure practices, failures are likely.

Read More: What Assets Can Be Tokenized?

Oracle Manipulation: Distorting the Truth

Oracle manipulation is a significant and often underestimated attack vector in decentralized finance (DeFi) that exploits the reliance of platforms on oracles for off-chain data, particularly cryptocurrency price feeds. Oracles serve as intermediaries, providing essential information that enables smart contracts to function properly. When oracles are compromised or manipulated, attackers can inject false data, leading to severe outcomes such as unjust liquidations, unauthorized asset minting, and distorted interest rates.

A notable example is the Mango Markets exploit in October 2022, where attackers manipulated prices to drain $117 million from the protocol. This incident underscores the risks associated with oracle manipulation, which has resulted in substantial losses across various DeFi platforms.

To mitigate these risks, it is crucial for DeFi protocols to enhance the robustness and decentralization of their oracle networks. Implementing secure and reliable oracles, along with careful selection based on market conditions, can help protect against these vulnerabilities. Ultimately, ensuring the integrity of oracle systems is vital for safeguarding users and maintaining trust in DeFi lending platforms.

Read More: What Assets Can Be Tokenized?

High Gas Fees and Network Congestion: Paying the Price of Popularity

One major risk in DeFi lending platforms, especially on Ethereum, is high gas fees during network congestion. These fees, which are paid to validators to process transactions, can surge when many users interact with the blockchain simultaneously. This makes basic actions like deposits and withdrawals costly, particularly affecting small lenders and borrowers by reducing returns and making loans less viable. Congestion also leads to transaction delays, increasing the risk of missing time-sensitive opportunities and making position management more difficult—similar to trying to process payments during rush hour when costs rise and delays are common.

Read More: What Assets Can Be Tokenized?

Counterparty Risk: Trust, But Verify (the Code)

Counterparty risk, while seemingly counterintuitive in the context of decentralized finance, still exists in DeFi lending, albeit in a different form than in traditional finance. While you are not directly relying on a centralized financial institution, you are still placing your trust in the code of the smart contract to function exactly as intended and on the borrowers to fulfill their repayment obligations (particularly in peer-to-peer lending models).

Undetected smart contract bugs can lead to unexpected failures, effectively making the code itself a potential counterparty risk. While over-collateralized lending reduces some of this risk by requiring collateral greater than the loan amount, it still depends on reliable liquidation mechanisms.In peer-to-peer DeFi lending, the risk of borrower default remains, mirroring traditional financial concerns. Ultimately, the risk shifts from institutions to code and protocol users, but the core concern — unmet obligations — persists.

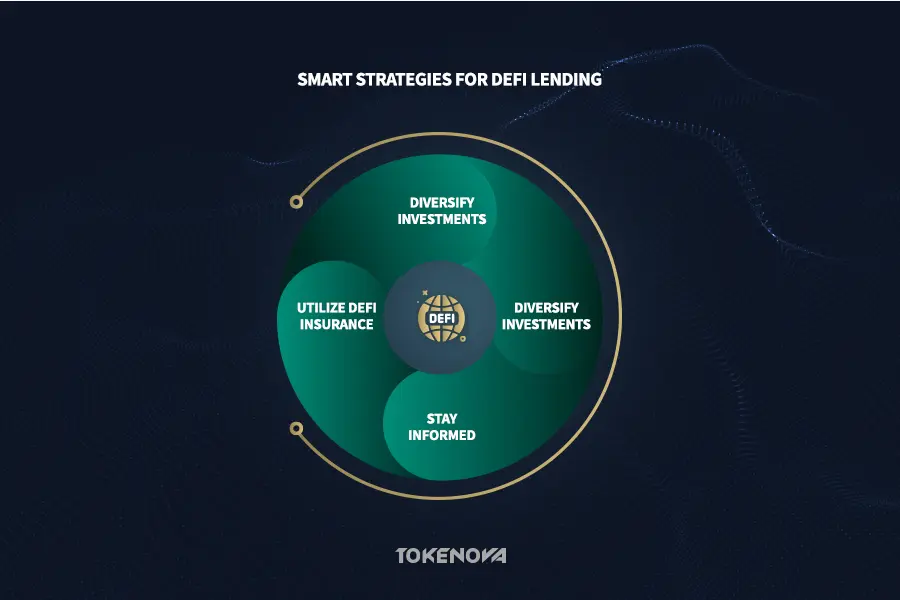

Mitigating DeFi Lending Risks: Playing it Smart

While the risks of DeFi lending platforms are real and warrant careful consideration, they are not insurmountable. Adopting a cautious, informed, and proactive approach is paramount to navigating this landscape successfully and safeguarding your investments. Here’s how to play it smart:

Platform Due Diligence: Know Where You’re Putting Your Money

Mitigating risk in DeFi lending starts with thorough due diligence. Investors should evaluate the platform’s team for transparency, experience, and credibility. Security is another priority—ensure the platform’s smart contracts have been audited by reputable firms like CertiK, PeckShield, or Trail of Bits, and review how any vulnerabilities were handled.

Examine the platform’s history for past exploits and assess the strength of its community, as an engaged and positive user base can indicate reliability. Tools like DeFi Pulse and DeFiLlama help compare platforms using metrics such as Total Value Locked (TVL), trading volume, and user activity. For example, in early 2025, Aave and Compound each had TVLs over $10 billion, reflecting their market leadership.

Just like in traditional finance, investing in DeFi lending platforms demands careful research into the platform’s fundamentals before committing funds.

Stay Informed: Your Best Defense

Staying informed about the ever-evolving DeFi landscape is an ongoing and essential responsibility for any participant. Keep a close watch on the latest news, emerging security vulnerabilities, and shifts in the regulatory environment. Follow reputable news sources dedicated to the cryptocurrency and DeFi space, such as CoinDesk, CoinTelegraph, and The Block.

Actively monitor the specific DeFi platforms you are utilizing for any announcements regarding protocol updates, potential security breaches, or changes to their operational mechanisms. Pay close attention to the activity within the liquidity pools you are participating in be aware of any significant or sudden shifts in liquidity or trading volume, as these could be indicators of potential issues. For example, in 2024, Ethereum-based DeFi platforms saw a huge increase in liquidity pool activity, driven by the rise of Layer-2 solutions like Arbitrum and Optimism.

Being proactive and well-informed allows you to adapt your strategies swiftly and potentially sidestep emerging risks before they impact your investments. Set up alerts for significant price movements or protocol changes related to your holdings to stay ahead of the curve. Think of it as staying updated on weather forecasts if you were planning a long journey being aware of potential storms allows you to adjust your route and avoid danger.

DeFi Insurance: A Safety Net in a Risky World

Consider utilizing DeFi insurance protocols as a strategic tool to hedge against specific risks inherent in DeFi lending. Platforms like Nexus Mutual and InsurAce offer insurance coverage for a range of potential adverse events, including smart contract failures, stablecoin de-pegging (when a stablecoin loses its peg to its intended fiat currency), and oracle exploits. While the DeFi insurance space is still relatively nascent and evolving, these protocols can provide an additional layer of financial protection and peace of mind for your investments.

For instance, Nexus Mutual has covered over $18 million in DeFi losses as of 2024, making it one of the most trusted insurance providers in the space. However, it’s crucial to thoroughly understand the terms and conditions of any insurance policies you consider, including what specific events are covered, the extent of the coverage, and any limitations or exclusions that may apply. Compare different insurance providers and their offerings carefully before making a decision, as coverage and premiums can vary. Think of it as purchasing insurance for your car or home it’s a cost incurred to mitigate potential financial losses from unforeseen circumstances.

Read More: What Assets Can Be Tokenized?

Start Small, Diversify Wisely: Don’t Put All Your Eggs in One Basket

To manage the risk of DeFi lending platforms effectively, start by investing only a small amount you’re willing to lose. This approach lets you learn how the platform works without facing major losses. Equally important is diversification—avoid putting all your funds into one platform or asset. Instead, spread your investments across multiple reputable platforms and asset types to reduce exposure to any single point of failure. Diversification helps minimize the overall impact if one platform fails or an asset drops in value.

For example, Coinlaw says: “The top five lending protocols—MakerDAO, Compound, Aave, Uniswap, and Curve—account for 84% of the DeFi lending market.”, but spreading investments across smaller platforms like Maple Finance and Euler can reduce exposure to single-platform risks. It’s a time-tested investment strategy that holds true in the world of DeFi as well don’t put all your eggs in one basket, especially in a nascent and volatile market.

By following these strategies, you can navigate the DeFi lending landscape with greater confidence and minimize potential risks. Always remember that in the dynamic world of decentralized finance, knowledge and caution are your most valuable assets.

DeFi vs. Traditional Lending: A Tale of Two Systems

When considering DeFi lending platforms, it’s crucial to weigh the potential high rewards against the significant risks. While DeFi can offer much higher returns than traditional financial products through methods like staking, yield farming, and liquidity provision, these gains come with elevated risks. The main risk factors include smart contract vulnerabilities, market volatility, and the experimental nature of DeFi technologies. Understanding these risks is essential before engaging with DeFi lending.

Conversely, traditional lending benefits from well-established regulatory frameworks designed to protect consumers and ensure financial stability. Robust institutional oversight, including central banks and regulatory bodies, provides a layer of scrutiny and accountability. Furthermore, the security offered by deposit insurance schemes, such as FDIC insurance in the United States, guarantees the safety of deposits up to a certain limit, mitigating the risk of loss due to bank failures. This structured environment offers a greater sense of security and stability for lenders and borrowers alike, albeit typically at the cost of lower yields on invested capital.

Key Distinctions in Operation and Features:

- Accessibility: DeFi platforms operate on permissionless blockchains, making them accessible to a global audience with an internet connection and a compatible cryptocurrency wallet. This eliminates the need for intermediaries like banks, potentially democratizing access to financial services for individuals who may be underserved by traditional systems. In contrast, traditional lending often involves Know Your Customer (KYC) and Anti-Money Laundering (AML) compliance, and access can be restricted based on geographical location, credit history, and other factors.

- Transparency: Transactions on DeFi platforms are typically recorded on a public blockchain, making them transparent and auditable. Anyone can view the transaction history, the amount of collateral locked in a protocol, and other relevant data. This inherent transparency can foster trust and accountability within the system. Traditional lending, while subject to regulatory reporting, generally involves less publicly accessible transaction data, and the inner workings of lending decisions can be less transparent to the average user.

- Risk Management: In DeFi, users bear a significant responsibility for their own risk management. Lending and borrowing often rely heavily on over-collateralization, meaning borrowers must provide collateral exceeding the value of the loan to mitigate the risk of default. Smart contracts automatically enforce these rules, and liquidations can occur if the collateral value falls below a certain threshold. Traditional lending systems employ a more structured approach to risk management, utilizing credit scores, loan officers, and various risk assessment models to evaluate borrowers’ creditworthiness and manage potential losses. Customer relationships and legal recourse also play a role in traditional lending risk management.

Ultimately, the decision to engage in DeFi lending or stick with traditional methods hinges on a nuanced understanding of individual risk tolerance, specific financial goals, and the level of familiarity with the underlying technologies and associated risks. It represents a fundamental trade-off between the potential for outsized gains, often accompanied by significant volatility and complexity, and the acceptance of the relative stability and security of traditional finance, albeit with potentially lower returns.

For instance, someone seeking high-growth potential and comfortable with navigating complex decentralized protocols might find DeFi appealing, while someone prioritizing capital preservation and seeking a predictable return might prefer the security of a traditional savings account.

The Future of DeFi Lending: Glimpsing What’s Ahead

The landscape of DeFi lending is in constant flux, characterized by rapid innovation and a persistent drive to overcome existing limitations while simultaneously bolstering security and enhancing the user experience. As we look towards 2025, several significant trends are poised to shape the future trajectory of this dynamic sector.

Key Trends in DeFi Lending

Cross-Chain Lending: A pivotal trend involves facilitating the seamless lending and borrowing of digital assets across disparate blockchain networks. This increased interoperability within the DeFi ecosystem promises to unlock significant liquidity, allowing users to access a wider array of assets and services regardless of the underlying blockchain. Imagine lending Ethereum-based assets and borrowing on a Solana-based platform, all within a unified experience. This interconnectedness is crucial for the continued growth and efficiency of DeFi lending.

Smart Contract Security Enhancements: Building unwavering trust in DeFi lending hinges on robust smart contract security. Ongoing advancements in this area are paramount. Techniques like formal verification, which employs mathematical proofs, are gaining traction to rigorously ensure the integrity and security of smart contracts. This proactive approach aims to drastically reduce the potential for exploits stemming from vulnerabilities in the code, offering greater assurance to users and investors alike.

Sophisticated Risk Assessment and Decentralized Insurance: The future of DeFi lending will likely see the emergence of more sophisticated risk assessment tools. These tools will be crucial for evaluating borrower creditworthiness in a decentralized manner and for managing collateral more effectively. Complementing this, decentralized insurance solutions are developing to provide a safety net against potential losses. This combination of better risk evaluation and insurance mechanisms will contribute to a more secure and resilient environment for all participants in DeFi lending.

The Impact of Regulatory Clarity: The evolving regulatory landscape will undoubtedly play a significant role in shaping DeFi lending. As regulatory frameworks become clearer and more defined, they may introduce certain constraints on operations. However, this clarity is also widely anticipated to foster greater stability within the sector and encourage broader mainstream adoption of DeFi lending platforms. A well-defined regulatory environment could be the key to attracting institutional investors who have, until now, been hesitant to enter the space due to compliance uncertainties.

Integration of Real-World Assets (RWAs): A particularly exciting trend is the increasing integration of real-world assets into DeFi protocols. This has the potential to unlock vast amounts of capital currently outside the DeFi ecosystem. Think of tokenized real estate, commodities, or even invoices being used as collateral or lent out on DeFi platforms. However, this trend also presents unique challenges related to accurately valuing these assets on-chain, establishing secure custody solutions, and navigating the complex legal frameworks that govern traditional assets4.

Growing Institutional Participation: The increasing engagement of traditional financial institutions with DeFi is a significant indicator of the sector’s growing maturity. The exploration of blockchain technology by firms like BlackRock and Deutsche Bank for their own operations signals a potential paradigm shift in how traditional finance interacts with decentralized systems. This trend could pave the way for innovative hybrid financial products that leverage the advantages of both DeFi and traditional finance, potentially bringing greater liquidity and stability to the DeFi lending space.

Read More: What Assets Can Be Tokenized?

Pro Tips for Safer DeFi Lending

Prioritize Hardware Wallets

Utilize hardware wallets to enhance the security of your interactions with DeFi platforms. Hardware wallets are physical devices that store your private keys offline, significantly reducing the risk of online attacks and unauthorized access compared to software wallets or leaving your funds on centralized exchanges. Consider using reputable hardware wallet brands like Ledger or Trezor and ensure you thoroughly understand how to properly secure and back up your recovery phrases this is your ultimate safeguard against losing access to your funds.

Scrutinize New Platforms

tential of DeFi with Tokenova

Struggling to navigate the complexities of DeFi? Let Tokenova guide you. As a leading advisory and consulting firm specializing in decentralized finance, we provide tailored solutions to help you thrive in the fast-evolving crypto landscape.

Scrutinize New Platforms

New DeFi lending protocols can promise eye-catching yields, but they often lack mature security, a long track record, and thorough audits. Investigate the founding team, demand proof of third-party code reviews, and verify past exploits (or their absence) before depositing funds.

Guard Against Phishing

Phishing remains rampant in crypto. Treat every unexpected email, link, or DM as suspect. Double-check URLs before connecting your wallet, never share seed phrases, and activate two-factor authentication to block unauthorized access.

Understand Leverage

Borrowing with leverage multiplies gains and losses. Know each platform’s liquidation thresholds and how fast collateral can be sold if prices turn. Use leverage only with clear risk limits and a plan for sudden market moves.

Unlock the Full Potential of DeFi with Tokenova

Struggling to navigate the complexities of DeFi? Let Tokenova guide you. As a leading advisory and consulting firm specializing in decentralized finance, we provide tailored solutions to help you thrive in the fast-evolving crypto landscape.

Why Choose Tokenova?

☑️Expert Guidance: Our team of blockchain and DeFi experts offers actionable insights to maximize your returns while minimizing risks.

☑️Custom Strategies: From portfolio diversification to risk management, we design strategies tailored to your goals.

☑️Smart Contract Audits: Ensure your investments are secure with our thorough smart contract reviews and vulnerability assessments.

☑️Regulatory Compliance: Stay ahead of the curve with up-to-date advice on global DeFi regulations.

☑️Insurance Solutions: Protect your assets with our partnerships with top DeFi insurance providers like Nexus Mutual and InsurAce.

Conclusion

DeFi lending offers exciting opportunities for passive income and involvement in next-generation finance, but it’s far from risk-free. Understanding the risks of DeFi lending platforms—including smart contract vulnerabilities, market volatility, impermanent loss, and regulatory uncertainty—is essential.

To manage these risks, users must stay informed, research platforms carefully, apply sound risk management strategies, and assess their personal risk tolerance. In the fast-moving DeFi space, knowledge and caution are key to minimizing downside and navigating the landscape safely.

Key Takeaways

- Smart contract vulnerabilities remain a primary gateway for exploits and financial losses in DeFi lending.

- Impermanent loss is an inherent risk for liquidity providers, potentially eroding returns.

- Regulatory uncertainty continues to cast a long shadow over the long-term prospects of DeFi platforms.

- Market volatility can trigger liquidations and significantly impact the profitability of both lending and borrowing.

- Thorough research, continuous monitoring, and diversification are indispensable strategies for mitigating risks in decentralized finance lending.

References:

Decoding DeFi lending: Motivations, risks, and investor behaviours

DeFi risks and the decentralisation illusion

Risk Management: DeFi Lending & Borrowing

Are DeFi lending platforms secure?

The security of DeFi lending platforms is not uniform and varies considerably from platform to platform. While some platforms implement robust security measures, undergo regular and rigorous audits by reputable security firms, and have established strong track records of secure operation, others may be more vulnerable to exploits and attacks due to less stringent security practices or unaudited code. Key factors to consider when assessing the security of a DeFi lending platform include its history of security incidents (or lack thereof), the quality and frequency of its smart contract audits, the transparency and reputation of its development team, and the overall level of engagement and security awareness within its community. It is absolutely crucial to conduct thorough due diligence on each individual platform before entrusting it with your valuable digital assets.

What is the role of collateral in DeFi lending?

Collateral plays a pivotal role in the mechanics of most DeFi lending platforms, particularly in over-collateralized lending models, which are the most prevalent. In these models, borrowers are required to provide assets as collateral, the value of which typically exceeds the value of the loan they are seeking. This over-collateralization acts as a crucial safety net for lenders, providing a buffer against potential borrower default or market fluctuations. If a borrower’s position becomes under-collateralized due to a decrease in the value of their collateral, the smart contract automatically initiates a liquidation process, selling off the collateral to repay the loan and protect the lenders from potential losses. The specific collateral requirements, the types of assets accepted as collateral, and the liquidation thresholds can vary significantly between different DeFi lending platforms, so it’s important to understand these parameters before participating.

How are DeFi lending interest rates determined?

Interest rates on DeFi lending platforms are generally determined algorithmically, based on the dynamic interplay of supply and demand within the specific liquidity pool for a given asset. When the demand for borrowing a particular asset is high, and the available supply of that asset for lending is relatively low, the interest rates offered to lenders tend to increase, reflecting the higher demand. Conversely, when the supply of an asset is abundant, and the demand for borrowing is low, interest rates for lenders typically decrease. This algorithmic determination of interest rates aims to create a market-driven and efficient system for balancing borrowing demand and lending supply. Some platforms also incorporate governance mechanisms that allow token holders to vote on or influence certain interest rate parameters, adding another layer of complexity to the rate-setting process.