Business tokenization turns ownership, access, or payments into digital tokens that can move and settle faster than traditional rails. In 2025, tokenization works best when you start with a real business goal, map clear token holder rights, and design compliance into the product. Jurisdictions with active pilots, stablecoin rules, and virtual asset licensing make token launches easier to scale.

Why tokenization looks different in 2025

State of Crypto 2025: The Latest Data, Trends, and Themes Revealed

Tokenization is no longer a “crypto experiment.” It is now a practical method for issuing digital representations of assets on trusted, programmable ledgers. Central banks and institutions are actively exploring tokenized money and tokenized settlement models.

At the same time, regulators are tightening standards. That is good news for serious builders. It pushes projects toward clearer disclosures, stronger controls, and real utility.

What you can tokenize (and what each token is for)

Use token types as product tools. Do not start with a token. Start with the job the token must do.

1) Payment tokens (stablecoins)

Best for: payments, settlement, treasury movement, on-chain commerce.

In the UAE, stablecoin-style “payment tokens” have defined expectations, including rules like “no interest paid to holders” in some structures.

2) Asset-backed tokens (real-world assets)

Best for: fractional ownership, faster transfer, broader investor access.

Real estate is a leading example. Dubai’s Land Department has launched a real estate tokenisation pilot and publicly projected that tokenised real estate could reach AED 60 billion by 2033, or about 7% of transactions.

3) Utility tokens

Best for: access, usage rights, in-app economies, network fees.

These work when utility is measurable and enforced inside the product.

4) Security tokens (regulated investment tokens)

Best for: equity-like or revenue-like exposure, fund interests, debt-like instruments.

These often require the most legal work, but they can unlock serious distribution.

5) NFTs (unique tokens)

Best for: unique ownership, tickets, memberships, collectibles, game items.

NFTs can still fall under financial rules depending on structure and marketing.

6) Governance tokens

Best for: voting, protocol decisions, treasury direction.

Governance only works when the decision scope is real and enforceable.

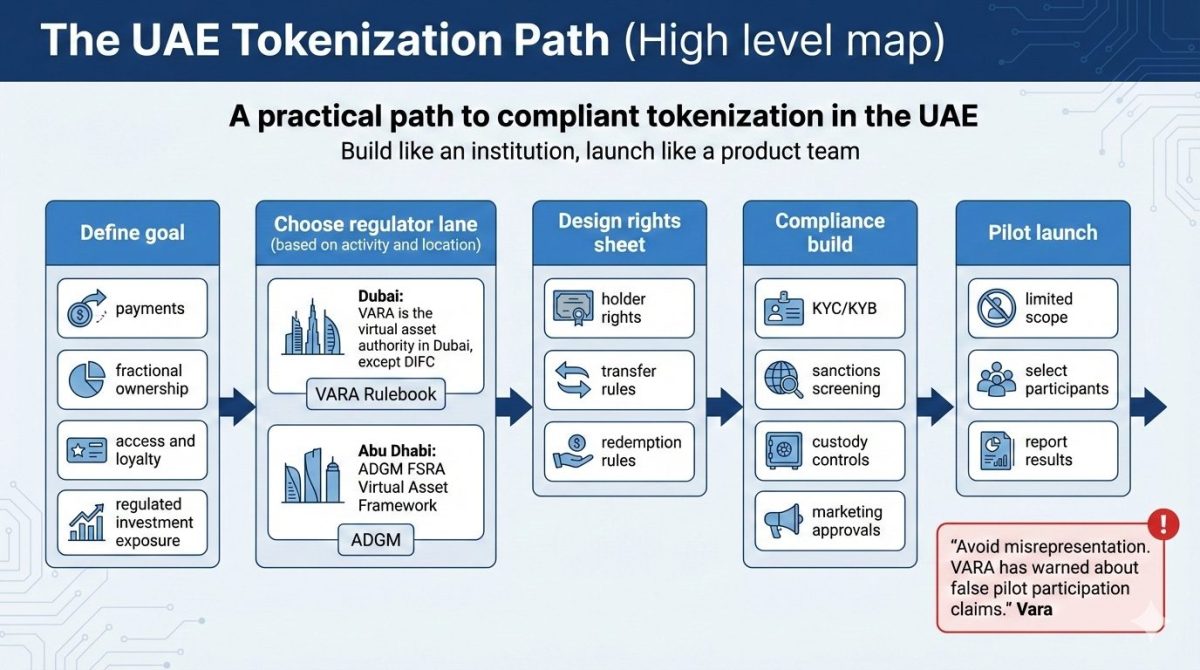

The “UAE advantage” without the hype

If you want a tokenized business that scales, you want three things:

- Clear regulators

- Clear rules for payment tokens and virtual asset activity

- Proof that real pilots exist

Dubai and Abu Dhabi have been building exactly that.

Dubai: real asset pilots and active enforcement signals

- Dubai Land Department launched a real estate tokenisation pilot, and published a long-term market projection.

- VARA publicly warned about firms falsely claiming participation in that pilot. This matters because it shows enforcement posture, not just marketing.

- VARA states it is the relevant authority for virtual assets across Dubai, except the DIFC free zone.

Abu Dhabi: regulated virtual asset framework and institutional products

ADGM’s FSRA Virtual Asset Framework encompasses areas such as AML/CFT, custody, disclosure, market abuse, and more. It also discusses how “stablecoins” may be treated depending on design.

Proof that tokenization is moving into mainstream finance

If you pitch tokenization to a CFO, show institutional examples.

- BNY + Goldman Sachs (July 2025): BNY announced that it will utilize blockchain technology from Goldman Sachs to maintain records of ownership for select money market funds.

- Tokenized money market funds are expanding: BIS describes tokenized MMFs as digital representations of regulated funds, and notes both traditional fund managers and crypto-native firms entering the space. It also explains allow-listing and permissioned transfer patterns.

- UAE real estate developer deal (January 2025): Reuters reported DAMAC signed a $1 billion deal with MANTRA to tokenize real-world assets.

- BlackRock BUIDL utility expansion (November 2025): Reporting and releases describe broader usage and integrations for the tokenized fund.

- ADGM example (October 2024): Reuters reported a tokenized U.S. Treasuries-themed fund launched in ADGM with regulatory approval.

Where tokenization creates real business value

Use this list as your “board slide.”

Value lever 1: Fractional access

You can lower minimum ticket sizes. This expands your buyer base.

Value lever 2: Faster settlement and simpler transfer logic

You can automate parts of ownership transfer, redemption, and reporting with smart contracts.

Value lever 3: New distribution

A token can be distributed via wallets, partner platforms, and compliant marketplaces.

Value lever 4: Better collateral and treasury tooling

Institutions are testing tokenized funds as collateral-like building blocks.

The Tokenization Blueprint (Step by Step)

Step 1: Pick one measurable goal

Examples:

- Raise capital for a specific asset pool

- Create a tokenized membership with paid access

- Enable compliant payments across partners

- Offer fractional exposure to a revenue stream

If your goal is vague, the token will fail.

Step 2: Define token holder rights in plain language

Write a one-page “rights sheet”:

- What holders get

- What holders do not get

- Transfer rules

- Redemption rules

- Fees

- Dispute process

If you are issuing a stablecoin-like product, do not imply central bank endorsement. Some issuer documents explicitly state that regulator review is not an endorsement of accuracy or completeness.

Step 3: Choose the regulated path before you choose the chain

In Dubai, virtual asset activity and marketing can be regulated and enforced. VARA has warned that even marketing real estate tokenisation services tied to Dubai assets may be unlicensed activity unless properly authorised.

In ADGM, the FSRA framework is detailed and expects strong controls.

Step 4: Decide if you need permissioned transfers

If you need compliance-grade transfers, design for allow-listed wallets and rules-based transfers. BIS explains how allow lists and token standards can enforce eligibility checks before transfers.

Step 5: Build the compliance stack

Minimum checklist:

- KYC/KYB and sanctions screening

- Wallet risk screening

- Market abuse monitoring if there is secondary trading

- Custody model and key management

- Marketing approvals and disclaimers

- Incident response plan

Step 6: Engineer token economics that match your business model

Keep it simple:

- Supply and issuance schedule

- Who receives tokens and why

- Lockups and vesting

- Redemption or buyback logic if relevant

- Fees and treasury rules

- Governance scope if governance exists

Step 7: Launch with a controlled distribution plan

Start with:

- A pilot user group

- A limited asset set

- Clear reporting

- A single primary market flow

Dubai’s real estate tokenisation pilot is explicitly described as “limited” with “select participants.” Treat that as the model for serious launches.

Use-case spotlight: gaming token economies

If you tokenize inside a consumer product, gaming remains a major on-chain category.

DappRadar’s Q3 2025 report states:

- 4.66 million daily unique active wallets in blockchain gaming

- Gaming was 25% of all active wallets in Web3, up from 20.1% in Q2 2025

- Gaming NFTs generated $135 million in trading volume in the quarter

Common mistakes to avoid (2025 edition)

- Claiming government or regulator participation you do not have

VARA issued a public alert about misrepresentation related to the DLD pilot. - Treating “stablecoin” as a marketing word

Stablecoins can trigger payment token rules, licensing, and strict reserve expectations. - Skipping permissioning and compliance when you need it

Allow-listing is not a “nice to have” for many real-world assets. - Overpromising yields

If your token economics depends on constant incentives, your risk profile rises fast.

Build the token like a regulated product, not a hype asset

Tokenization in 2025 is about turning a real business function into a programmable and auditable asset. The winners start with one clear outcome, like faster settlement, fractional access, or a better membership model. Then they map rights and restrictions in plain language. They choose the regulatory lane early. They build KYC, custody, and marketing controls into the stack. That is how tokenized models earn trust and scale.

If you want a strong base for global growth, build where pilots are real and rules are clear. Dubai’s real estate tokenisation pilot and the region’s active supervision signal a market that is serious about execution, not slogans. Pair that with disciplined tokenomics and a controlled launch, and tokenization becomes a durable advantage.

FAQ (AEO-focused)

What is tokenization in simple terms?

Tokenization is issuing a digital token that represents a right, asset, or access rule on a programmable ledger.

Is tokenization legal in the UAE?

It depends on the activity, location, and regulator lane. Dubai and ADGM have defined virtual asset frameworks, plus active enforcement signals.

What is the fastest token model to ship?

Utility or membership tokens are often fastest. They still require clean disclosures and compliant marketing.

What token model is best for real estate?

Asset-backed tokens with clear ownership and transfer rules. Dubai’s DLD pilot is a key market signal.

Do I need allow-listed wallets?

If transfers must be restricted to eligible users, allow-listing is often required. BIS describes how this works in tokenized fund models.

What is the biggest risk in tokenization?

Misaligned promises. That includes unclear rights, weak compliance, or implied endorsements.

What is a strong 2025 proof point for tokenization?

BNY and Goldman Sachs working on tokenized MMF ownership records is a strong institutional signal.

Why are regulators focused on stablecoins?

Because they can scale quickly and affect payments and financial stability. Major policy bodies have warned about risks without strong regulation.