There was a time when some people treated stablecoins like a pitch deck with a peg.

ADGM did not get the memo.

As of January 1, 2026, the Abu Dhabi Global Market framework for Fiat-Referenced Tokens, or FRTs, is much wider and much sharper. It is not just about issuing a token anymore. It also covers how regulated firms can use FRTs, intermediate them, and hold client FRTs inside regulated activity. ADGM’s FSRA said exactly that when it finalized the 2025 amendments that took effect in 2026.

For builders, that means one thing. Your product is now part treasury system, part disclosure engine, part compliance machine.

For operators, it means shortcuts are off the menu.

And for market participants across the UAE, especially the quiet capital that prefers clean structures over noisy headlines, it means ADGM is treating fiat-linked tokens like financial products with real obligations, not digital lucky charms. ADGM first introduced the dedicated issuance framework in December 2024, then expanded it in 2025, with the broader regime effective from January 1, 2026.

Executive takeaway

The core idea is simple.

If your business touches an FRT inside a regulated activity in ADGM, the regulator expects real discipline around redemption, reserves, disclosures, and token acceptance. It also expects firms to use only Accepted Fiat-Referenced Tokens when they carry on a regulated activity involving FRTs. ADGM says that clearly in both its Digital Assets page and the COBS rulebook.

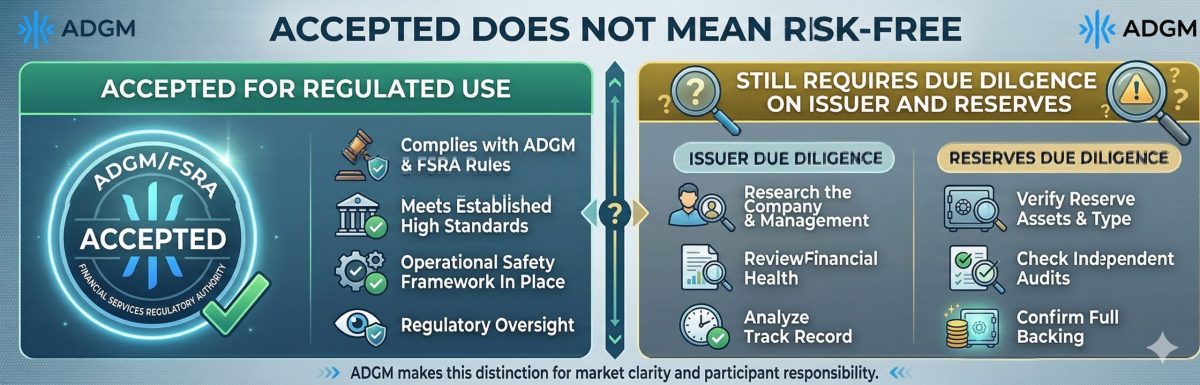

That “Accepted” label matters. But it is not a halo.

ADGM explicitly says that inclusion on the Accepted FRT list does not remove the need for independent due diligence on the issuer, including creditworthiness and reserve composition. In plain English, accepted does not mean harmless. It means admitted. There is a difference, and good investors know it.

Why ADGM’s FRT rules matter now

ADGM has built a dedicated framework for FRT issuance and then extended that framework into a broader operating regime. The 2025 finalization introduced an approach to “accepting” FRTs, expanded the regulated activities that may be carried on in relation to FRTs, and added rules for firms that hold or control client FRTs.

This matters because the market still uses the word “stablecoin” loosely. ADGM does not. Its guidance makes clear that an FRT is a specific category. It is a digital asset linked to a single fiat currency and redeemable with the issuer on demand. Not every asset marketed as a stablecoin fits that definition.

That detail is not academic. It decides whether your design belongs inside the regime or outside it.

The 2026 rulebook, minus the fog

1. Issuance is a regulated activity, not a mint button

ADGM’s 2024 framework made issuing a Fiat-Referenced Token a distinct regulated activity. It also set the tone. White papers are not decorative PDFs. They are part of the regulatory architecture. The framework introduced disclosure duties, reserve standards, stress testing, prudential safeguards, and redemption rights.

There is also a structural limit that builders should not ignore. An issuer of an FRT is prohibited from carrying on additional regulated activities that are not incidental to issuance. So the “one entity does everything” dream gets expensive, fast. Group structuring starts looking less like legal overhead and more like survival math.

2. Redemption is a promise with a stopwatch

ADGM does not treat redemption like a vague customer support aspiration.

Under COBS 19A.4.1, an issuer must issue FRTs at par value without delay upon receipt of money. It must also redeem FRTs at par value no later than T+2 after customer due diligence is completed, where due diligence is required. Redemption must be paid in the fiat currency to which the token is referenced. Any redemption fee must be proportionate to actual costs and stated in the white paper.

That rule alone changes product design. Your redemption flow is not just UX. It is compliance in a user interface.

3. Reserves must behave like reserves

ADGM’s framework is strict on reserve integrity. The point is not just that reserves exist. The point is that they remain sufficient, traceable, and operationally useful when stress hits.

Issuers must ensure that the combined market value of reserve assets is always equal to or greater than outstanding redemption claims. They must conduct a valuation of reserve assets by the end of each day and notify the regulator immediately if they are, or suspect they may be, in breach.

The framework also requires segregation where an issuer has more than one FRT. Reserve assets for each FRT must be kept separate from the others. Before materially changing reserve composition, the issuer must notify the regulator in writing and explain why. The regulator can also direct the issuer to divest reserve investments and move proceeds into a client account.

In other words, “trust us, bro” has officially failed onboarding.

4. Stress testing and attestation are not optional extras

Issuers must have systems to regularly stress test reserve composition and the market and counterparty risks that could create a shortfall. These stress tests must be performed at least annually and must include liquidity stress scenarios such as large-scale redemptions. A written summary must be provided to the regulator.

Then comes the monthly proof.

Under COBS 19A.9.1 and 19A.9.2, an issuer must prepare a monthly written attestation by an independent third party approved by the regulator. The attestation must state the amount of relevant money held, the market value of reserve investments, the total par value of outstanding FRTs, and whether reserves plus relevant money equal or exceed redemption value. It must be published on the issuer’s website and submitted to the regulator by the end of the following month.

That is not marketing transparency. That is operational transparency on a schedule.

5. Annual audits are part of the package

ADGM also requires an annual audit of reserve composition, valuation, and the issuer’s internal controls and compliance arrangements for reserve management. The audit must be performed by an independent external auditor approved by the regulator. It must be addressed to both the issuer and the regulator, and submitted within four months after the end of the issuer’s financial year.

A missing monthly attestation is bad.

A sloppy annual audit is worse.

6. Only Accepted FRTs can be used in regulated activity

This is the practical gate that many operators care about most.

COBS 17.2A.1 says that an authorized person or recognized body carrying on a regulated activity involving an FRT must only use Accepted Fiat-Referenced Tokens. The related guidance makes clear that this applies across transfers, safekeeping, and payments involving the firm.

ADGM’s Digital Assets page says the same thing and adds the important warning that the Accepted FRT list may change over time.

So if a business wants to use an FRT for settlement, custody, or payment flows inside regulated activity, “close enough” is not a strategy. It is a future incident report.

What changed in 2026

The big 2026 shift is scope.

The 2024 regime focused on issuance. The 2025 amendments, effective from January 1, 2026, expanded the framework to cover regulated activities involving FRTs more broadly, including an FSRA approach to accepted FRTs and rules for firms that hold or control client FRTs.

ADGM also states that there is a defined lane called Fiat-Referenced Token Intermediation within the broader 2026 framework. That matters for brokers, payment firms, exchanges, and any platform that thinks it is “just helping users buy and sell.” The regulator has heard that line before.

What builders should do now

Build compliance into the product, not around it

If your white paper says redemption at par, your treasury, banking rails, controls, and customer flow all need to support that claim in real time. ADGM’s rules do not reward poetic ambition. They reward operational alignment.

Treat the white paper like a control document

Every statement in the white paper can become a future question from a regulator, a banking partner, or a due diligence team. That is why vague white papers age badly. The market may forgive them. The rulebook will not. ADGM’s 2024 framework made disclosure a core pillar of FRT issuance.

Design treasury like infrastructure

Daily valuation, monthly attestation, annual audit, and reserve change notices all mean one thing. Treasury is not a back office. Treasury is the product’s spine.

Keep the entity map clean

If the issuer also wants to do ten other things, the structure needs to reflect the regulatory boundaries. ADGM is not telling firms to be boring. It is telling them to stop pretending that legal structure is optional.

What operators should do now

Add an Accepted FRT gate to listings and integrations

If the business is regulated and the token is an FRT, only Accepted FRTs can be used. That should sit in listing memos, settlement policies, custody approvals, and payment playbooks.

Monitor issuer reporting like a credit product

Monthly attestation. Annual audit. Daily reserve sufficiency checks. These are not passive documents. They are live risk signals. Operators should track them like a bank tracks counterparty data.

Do not confuse “accepted” with “safe”

ADGM literally warns firms and holders to do their own assessment of the issuer and the reserves. If an operator hides behind the accepted label and skips the rest, that is not prudence. That is cosplay.

The investor lens, especially in the UAE

For the more discreet side of the regional market, the smart question is no longer “is there a stablecoin angle?”

The better question is “what is the legal and operational quality of the FRT model?”

ADGM’s regime gives investors a cleaner checklist. Ask whether the token is accepted for use in regulated activity. Ask how redemption really works. Ask who holds the reserves. Ask whether monthly attestations are published on time. Ask how reserve composition is managed. Ask whether the annual audit has been delivered. ADGM’s own rules and public guidance make those questions relevant, not optional.

In short, the region is not short on ambition.

The differentiator now is boring excellence.

That is usually where the real money gets comfortable.

Everyone Deserves Stability

ADGM’s 2026 Fiat-Referenced Token rules are not anti-innovation. They are anti-hand-waving. If your token touches regulated activity, the real game is reserves, redemption, attestations, and accepted-token status.

FAQ

What is a Fiat-Referenced Token in ADGM?

In ADGM, a Fiat-Referenced Token is a digital asset linked to a fixed amount of a single fiat currency and redeemable from its issuer on demand. ADGM treats FRTs as a specific regulated category, not as a casual catch-all for stablecoins.

Can firms in ADGM use any stablecoin in regulated activity?

No. An authorized person or recognized body carrying on a regulated activity involving an FRT must only use Accepted Fiat-Referenced Tokens.

What are ADGM’s redemption rules for FRT issuers?

Issuers must issue at par without delay and redeem at par no later than T+2 after customer due diligence is completed, where due diligence is required. Redemption must be paid in the referenced fiat currency.

Does accepted status mean an FRT is risk-free?

No. ADGM says inclusion on the Accepted FRT list does not remove the need for independent due diligence on the issuer, including creditworthiness and reserve composition.

What reserve disclosures do ADGM FRT issuers need to publish?

Issuers must prepare a monthly attestation by an independent third party approved by the regulator and publish it on their website. They also face annual audit requirements.